It has become clear to us at the Board of Pensions that a one-size-fits-all benefits plan may have had a certain appeal to an egalitarian sentiment, but in reality such a plan meets the needs of some but excludes many more. For the last four years, the Board has been engaged with the denomination at all levels to find out what is needed and then worked to structure support within our legal and financial constraints.

The Board has dramatically expanded its flexibility and has succeeded in increasing the number of active members in the Benefits Plan by nearly 25% over the last two years. For the first time, the plan serves more employees who are not ministers than ministers themselves. This is healthy growth. However, this article concerns the unique needs of, and support for, ministers and others who are leading congregations.

Presbyterian ministers serving traditional congregations

The Presbyterian Church (U.S.A.) is disappearing, emerging and thriving — all at the same time. Our research has found three distinct groups of congregations:

Small and declining: These churches often face demographic and geographic challenges they will never overcome. These congregations number 150 or fewer members. Approximately 40% have installed pastoral leadership. They represent approximately 75% of our churches, but just over a quarter of our PC(USA) church members.

Small and stable or emerging and growing: Like the first category, these congregations have fewer than 150 members but have found a core sustainability. These include many of our 1001 New Worshipping Communities (numbering 455 as of December 31, 2018) and congregations that have a stable source of income that is often greater than annual giving, such as an endowment.

Small and stable or emerging and growing: Like the first category, these congregations have fewer than 150 members but have found a core sustainability. These include many of our 1001 New Worshipping Communities (numbering 455 as of December 31, 2018) and congregations that have a stable source of income that is often greater than annual giving, such as an endowment.

Large churches: These are churches with more than 150 members. They almost always have an installed pastor, a sanctuary and a more or less balanced budget. Many of them enjoy dynamic mission, programming and worship. Often they are growing in membership, and 72% of PC(USA) church members belong to one of these congregations.

In fact, if one applies the three criteria cited for large churches (pastor, sanctuary, sufficient budget) to all churches regardless of size, one finds that 84% of all Presbyterians experience church in this way, making it the overwhelming expression of Presbyterianism in the United States.

For installed ministers, all of whom remain enrolled in full benefits through Pastor’s Participation, the system is still working quite well. The Board has recognized that the same is not true for the ministers and/or congregations who do not fit this profile, and thus created dramatic flexibility in the Benefits Plan and incentives to facilitate different solutions in different contexts of ministry.

Expanding choice and access

The first (and most important) step was to unbundle the benefits package in such a way that congregations and non-installed ministers could choose which benefits best fit their context, structurally and financially. If one is to make rational choices, one must know the actual cost, so the Board has moved to transparent pricing at actual cost for its menu options.

All employees of any congregation who are scheduled to work at least 20 hours per week are eligible to obtain benefits. That includes non-installed ministers (interim, stated supply, contract, etc.) and commissioned pastors (formerly known as commissioned lay pastors or commissioned ruling elders). Non-installed ministers of Word and Sacrament who earn income from the practice of ministry may declare themselves self-employed and buy certain benefits directly.

True choice does not mean a “yes” or “no” answer to a single offering, as things were in the past. Now, for example, menu participants choose the tier of medical coverage that they need (employee only, employee and spouse, employee and children, employee and family) from one of three medical coverage options at different price points.

Medical coverage options

Each coverage option provides access to the Blue Cross Blue Shield (BCBS) network of physicians, hospitals and other healthcare providers — the largest in the country. All include prescription drug coverage, as well as access to the Board’s wellness initiative (Call to Health) and the Employee Assistance Program (EAP):

The preferred provider organization (PPO): This health option provides the greatest benefits, and includes a sliding scale deductible based on salary to honor our community nature. It pays out-of-network claims for most providers. Participants can lower their deductibles by one-third when completing Call to Health.

The exclusive provider organization (EPO): The EPO is priced approximately 15% below the PPO. It has no out-of-network benefits and requires certain prescriptions be filled with generics. Certain benefits are not available, including the sliding scale deductible. However, participants can lower their deductibles by 25% when completing Call to Health.

The high deductible health plan (HDHP): The HDHP is priced about 21% below the PPO and, like other high deductible plans, includes access to a health savings account (HSA). Unlike almost any other high deductible plan, the HDHP utilizes the national BlueCard network and includes significant preventive care and prescription drug coverage, and a 25% reduction in deductibles with completion of Call to Health.

While medical coverage is usually the most costly element of protecting our employees from undue risk, other benefits should not be overlooked. The Pension Plan, Death and Disability Plan and Retirement Savings Plan (RSP) of the PC(USA) have all been included in the menu.

Other menu choices

Pension Plan: This is a defined benefit plan for which the dues are 11% of effective salary. The dues must be paid entirely by the employer. The plan includes important community nature provisions, such as accruing the pension at the higher of the actual effective salary or median effective salary for the employee category. Many small-church pastors retire without seeing income decline. Additionally, 20 years of Pension Plan participation makes retirees and their surviving spouses eligible for the Board’s income and housing subsidies if their income does not equal 65 percent or more of the current median effective salary for pastors.

Death and Disability Plan: This is included with the pension for an additional 1% of effective salary, paid by the congregation. It provides important coverage not available in the commercial market. Once disabled, a covered member will continue to accrue pension until normal retirement age. If receiving medical coverage through the Board, the member’s coverage continues until Medicare-eligibility age. Upon death, in addition to a lump-sum benefit, this plan includes one year of salary continuation for the spouse and $40,000 for the post-secondary education of each minor child. A congregation can provide Death and Disability Plan coverage without pension at a cost of 2.5% of effective salary.

Retirement Savings Plan of the PC(USA): The RSP is a 403(b)(9) savings plan similar to a 401(k). However, the size and scope of the Board have allowed it to negotiate extremely low fees for account maintenance (currently $15/year/participant) and institutional fees for all of the investment choices. No comparable pricing can be negotiated on a small-employer basis. No employer match is required (but is certainly encouraged). There is no minimum hourly workweek required for RSP participation.

Optional programs: The Board offers a wide range of optional benefits that employers may offer, but that require no employer contribution. These include supplemental death and disability coverage for added income protection, dental and vision eyewear coverage, group life insurance, flexible spending accounts and educational resources.

Special programs for employers

Special programs for employers

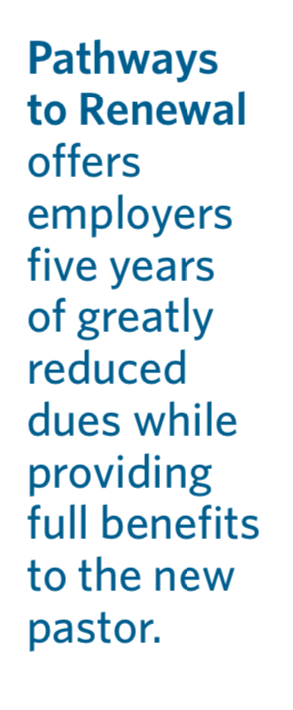

In July 2018, the Board launched a pilot program to invite small churches without a pastor for two years or new innovative ministries to call and install new pastors. Pathways to Renewal offers employers five years of greatly reduced dues while providing full benefits to the new pastor. The newly employed minister must be under 40 and never previously enrolled in Pastor’s Participation. To be eligible for Pathways, a congregation:

- Must have membership of 150 or fewer, not had an installed pastor for at least two years and not elected a Pastor Nominating Committee; or

- Have a membership of any size and use Pastor’s Participation to expand ministerial headcount.

The Board of Directors recently approved another initiative to provide presbyteries that employ organizing pastors and evangelists (job code 301) with deeply subsidized dues while providing full benefits to the organizing minister. Here are the criteria:

- The minister is employed by the presbytery for no less than 20 hours per week.

- The minister has an effective salary that is less than the median for pastors.

- The minister is not currently enrolled in Pastor’s Participation and has not been enrolled for Pastor’s Participation in this employment relationship, or with this employer, for at least two years prior to enrollment through this initiative.

- The minister has not initiated a retirement benefit with the Board of Pensions.

Additional support for ministers

With the budget approved by the 223rd General Assembly (2018), the denominational support program for newly ordained ministers was eliminated. To step into that gap, the Board expanded its CREDO program from mid-career pastors to include all newly ordained ministers in the Benefits Plan. While most CREDO participants go for a week of discernment led by expert faculty in the areas of finance, spirituality, vocation and health, the newly ordained participants attend two weeklong gatherings, a year apart. At the other end of ministry’s arc, we offer CREDO II for those who see themselves in their last chapter of full-time ministry.

With the budget approved by the 223rd General Assembly (2018), the denominational support program for newly ordained ministers was eliminated. To step into that gap, the Board expanded its CREDO program from mid-career pastors to include all newly ordained ministers in the Benefits Plan. While most CREDO participants go for a week of discernment led by expert faculty in the areas of finance, spirituality, vocation and health, the newly ordained participants attend two weeklong gatherings, a year apart. At the other end of ministry’s arc, we offer CREDO II for those who see themselves in their last chapter of full-time ministry.

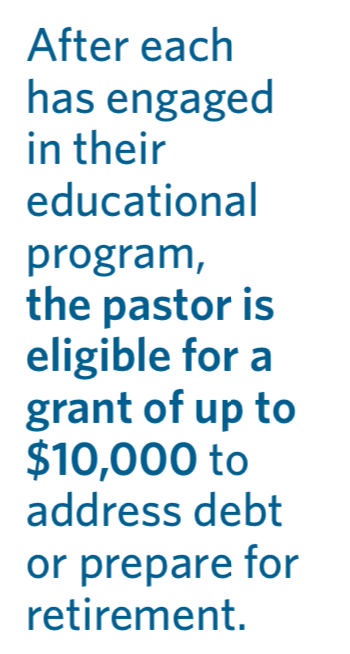

Recognizing that financial strains on ministers come in many forms, the Board has developed Healthy Pastors, Healthy Congregations (HPHC). This program is designed to help pastors with financial literacy and congregations with understanding the financial stresses of ministry. After each has engaged in their educational program, the pastor is eligible for a grant of up to $10,000 to address debt or prepare for retirement. The program is being funded by $4 million from the Board and a $1 million commitment from Lilly Endowment.

About half of new ministers are carrying a substantial educational debt load. The Board has increased assistance to any of them who have completed either HPHC or CREDO. There is now $25,000 available, tax-free based on need, to relieve debt and help stabilize our ministers in their calls.

Case studies

Sarah

Sarah is in her final year at seminary and looking for her first call. If she believes she can only find a part-time call and must combine it with a secular job, she will limit her search to those larger cities where dual employment is more likely.

Likewise, if First Presbyterian Church of Anywhere believes that its time has passed and that it will never call a minister again, it may not even call a PNC and fill out its MIF.

Likewise, if First Presbyterian Church of Anywhere believes that its time has passed and that it will never call a minister again, it may not even call a PNC and fill out its MIF.

But First Presbyterian has a manse, and maybe it can afford $40,000 a year in cash salary. Using Pathways to Renewal, the annual dues to the Board would be less than $8,000 per year. All in, that’s $4,000 a month out-of-pocket. If Sarah knew she would be solo pastor for five years, accrue pension credits and have a place to live, medical coverage, the Assistance Program backing her up in a financial crisis, a guaranteed spot in CREDO for newly ordained pastors and the chance to pay off $25,000 in student loans tax-free, do you think she would be interested?

Ben

Ben is ministering 20 hours a week to a small congregation as a commissioned pastor. He has heard God’s strong call and is working toward an M.Div. in an online-based seminary distance education program, but knows it will take at least five years. His wife has a job in town, but her medical coverage is employee-only. Picking up a spouse or child is really expensive on her policy. Ben’s part-time work doesn’t provide benefits but pays him pretty well. His church wants to help out but doesn’t know the best way.

For $7,000 to $8,000, Ben can get medical coverage for himself through the Board, splitting the cost with the church. They decide to go with the EPO and each pay $300 a month. Ben can choose to enroll his children at an additional cost. If healthcare coverage is all the church can manage, Ben can still sign up for the RSP and begin tax-deferred savings. If the church has a little extra, they can get Ben enrolled in pension and death and disability coverage for the minimum of $157.75 per month.

Go to pensions.org to find all the ways the Board is helping, or call 800-773-7752 (800-PRESPLAN). There are lots of ways the Board can help support those leading God’s people.

FRANK SPENCER is the president of the Board of Pensions of the Presbyterian Church (U.S.A.).